JACKSONVILLE, Fla. — An Action News Jax investigation reveals disparities in how much you pay for car insurance in Florida based on your gender, credit score and where you live. We analyzed tens of thousands of lines of insurance data and discovered your driving history is only a very small factor in how you’re charged.

There is no shortage of drivers on Jacksonville roads and no shortage of drivers willing to give Action News Jax their “two cents” about the cost of car insurance.

Driver Easter Gibbons said, “I have Geico and my insurance went up and I asked why?”

Driver Michael Schornak said, “You don’t need it until you need it, and I think insurance is way too high.”

>>More Action News Jax Investigates

The nonprofit Consumer Federation of America is raising concerns about how insurance companies determine what you pay.

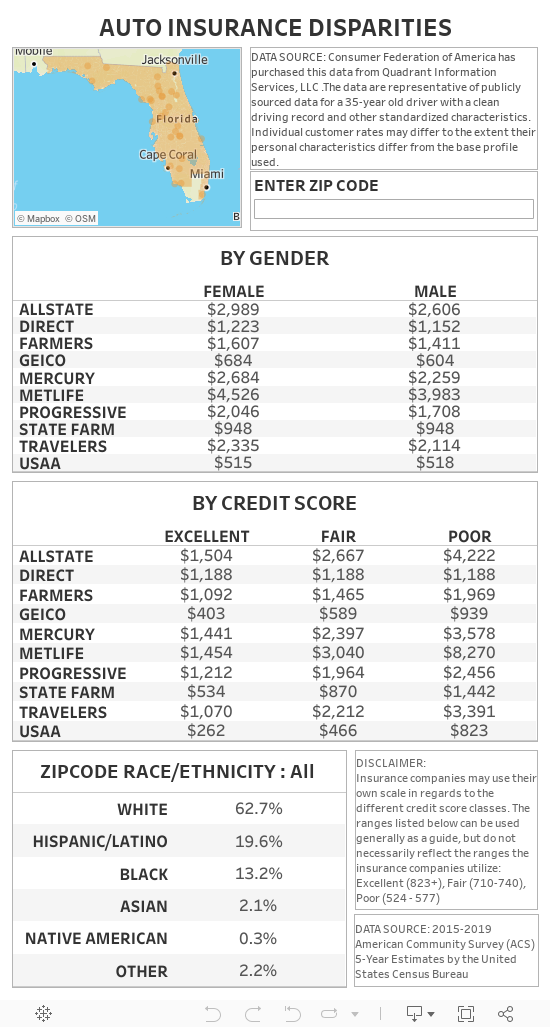

The CFA gave Action News Jax pricing data it obtained from Quadrant Information Services, LLC. The data detailed annual insurance premiums from the 10 largest insurance carriers in Florida.

Doug Heller with the CFA said, “I want the insurance companies to be on notice that we’re watching their behavior.”

Heller said the data given to Action News Jax is from Florida drivers that are 35 years old, drive the most common car—a 2011 Honda Civic EX, drive 10 miles to work each day and had perfect driving records.

What differed was their gender, credit rating and zip code where they lived. Heller, who has worked on insurance issues for more than 20 years, says they found some disparities.

“The pain of unfair pricing in the Florida auto insurance market kind of accumulates on poor communities, communities of color in particular and then made even worse for women.” Heller also said, “We also found that if you look at people’s credit history the penalty for having low credit is excruciating, we’re talking thousands of dollars a year or more for auto insurance.”

Action News Jax created a tool that you can use to see price disparities Heller found in his research. The tool shows you how much you would pay for each company based on where you live, your gender and your credit score.

You can use that tool at the bottom of this story.

At a glance, the CFA determined on average women in Florida pay around $220 more than men and people with poor credit paid around $1800 more than people with excellent credit.

Heller said, “There is really no good excuse for insurance companies using credit, but they like it because it allows them to slice and dice the market so they can find the customers that have more wealth and more financial stability, because they think they’re going to be able to sell them more products.”

Heller said the data also shows some zip codes with higher populations of black residents appear to have higher rates than zip codes with majority white residents.

Heller said, “You could almost map the old history of racist housing policy onto the current maps of auto insurance prices and it would look the same, so there’s no way that just kind of happened. That’s not just random. That’s the roots of institutional racism playing out in the premiums we pay for auto insurance.”

Mark Friedlander with the Insurance Information Institute disputes the CFA’s findings that there are price disparities for Florida auto insurance premiums by gender, zip code or credit rating.

“The process seems flawed to us.” Friedlander also said, “It doesn’t add up what they are showing here.”

Friedlander said statistics show why credit scores matter with pricing.

He said, “For simple terms we’ll call it your insurance score. Those that have higher scores are safer drivers and less chance of having and accident and filing a claim. Those with lower credit scores will have more of a chance of being in an accident and filing a claim.”

Friedlander said the Insurance Information Institute’s research also shows women pay less than men — not more.

Friedlander said, “They get into fewer accidents, they have fewer dui violations and most importantly they have less serious accidents.”

Action News Jax also asked Friedlander how zip code and race factored into pricing. “The way insurers look at this is, they determine your location and they look at data like rate of theft, vandalism and accidents in a particular area and they rate each zip code according to those factors.”

Friedlander also said, “The other thing I really want to point out is it’s illegal for insurers to determine rate based on race or ethnicity.”

Friedlander did tell Action News Jax the National Association of Insurance Commissioners formed a task force to look into all the criteria insurers use.

Friedlander said, “One of the reasons why they have this formula of a dozen of more rating factors is to avoid scenarios like that. They don’t want to be in a position where an underwriter is being accused of being prejudice towards one driver over another or favoring one area of a community versus the other.”

Heller stands by the Consumer Federation of America’s findings and says he will keep pushing insurance companies and lawmakers to level the playing field.

Florida law requires drivers to have insurance, so Action News Jax reached out to lawmakers to find out their role in ensuring fair pricing.

State Senator Audrey Gibson, who represents Jacksonville, said she supports using data to determine rates for drivers.

Gibson said, “But not anything egregious that is totally driven by zip code or race or gender for that matter. And the legislature has a duty to make sure that that’s not happening.”

Many drivers like Britney Kushma wish it were simpler. “It should just be based off of how you drive your car.” Friedlander with the Insurance Information Institute said it’s more complicated than that — otherwise insurance companies wouldn’t be able to pay out for crashes and stay in business. Friedlander said, “There are many factors that determine you know what type of driver you are and just driving history isn’t enough.”

Local News: Understanding the child tax credit: Who will get it and for how long

While there’s debate around what should factor into how much you pay, nearly everyone Action News Jax talked to agreed on what you can do to save money — shop around. Heller said, “You spend an hour, you will almost certainly save yourself $100 or $200 dollars on your rates.”

There is a bill on Florida Governor Ron DeSantis’ desk that would require drivers to carry bodily injury coverage instead of personal injury protection.

Supporters say it would help bring rates down and prevent fraud. But critics think it could make auto insurance more expensive — creating challenges for low-income drivers and leading to more uninsured drivers on the road.

Below you can use the tool that Action News Jax created to see price disparities, which also includes the data from the Consumer Federation of America.

Cox Media Group